In a ruling dated October 7, 2011 (BIR

Ruling No. 370-2011), the Philippine Bureau of Internal Revenue (BIR)

ruled that “the PHP 24.3 billion discount on the issuance of the

PEACe Bonds should be subject to 20% Final Tax on the interest income

from deposit substitutes,” as provided in Section 27(D)(1) of the

TaxCode of 1997.

This ruling reversed three previous BIR

Rulings made under former BIR Commissioner Rene G. Banez of the

Arroyo Administration on the PEACe Bonds issued in 2001. (No.

020-2001 dated May 31, 2001 and No. 035-2001 dated August 16, 2001

and No. DA-175-01 dated September 29, 2001).

Rulings under the Negotiated Sale

Mode of Purchase

The May 31 and August 16 rulings were

made at the time that CODE-NGO was attempting to enter into a

negotiated sale of the PEACe Bonds with the Bureau of Treasury. Under

this scenario, the bonds would be sold by the government to a single

entity, RCBC (as a Government Securities Eligible Dealer or GSED) who

would then resell the bonds to another single entity, CODE-NGO.

CODE-NGO would then simultaneously resell the bonds to RCBC Capital

(with a firm underwriting commitment from RCBC Capital).

The May 31, 2001 ruling said that the

PEACe Bonds were not considered to be a “public” borrowing, even

if the bonds would fund the government, because the PEACe Bonds were

to be issued to a single entity, CODE-NGO. Since the bonds complied

with the “19-Lender Rule,” the bonds were not to be classified as

“deposit substitutes.” Under Section 22 (Y) of the 1997 Tax Code,

the borrowing of funds can be classified as deposit substitutes “if

the funds are obtained from twenty (20) or more individuals or

corporate lenders at any one time.”

However, lingering questions remained

on the meaning of the word “public” and the interpretation of the

phrase “at any one time.” Hence, there was a need for a second

clarificatory ruling on August 16, 2001. The ruling stated that

since the bonds will be “issued only to one entity, that is, RCBC,”

there is no borrowing from the public. The ruling also stated that

“the phrase 'at any one time' covers only the origination or

original issuance of the bonds regardless of whether sale or trading

is made in the secondary market.” This ruling effectively allowed

RCBC/RCBC Capital to resell the bonds in the secondary market without

losing the tax-exempt status of the bonds.

However, the ruling required that

CODE-NGO/RCBC warrant that it is acquiring the bond for its own

behalf. The ruling stated that:

“a

representation or warranty should be made to the effect that the

bonds are acquired upon their original issuance by the original

purchaser thereof, for and on its own behalf, or on behalf of a

single purchaser only, and in the latter case, that the purchaser is

acquiring such bonds for its own account and not for the account of

other entities.”

Ruling under Treasury Bond

Auction Mode of Purchase

CODE-NGO's proposed mode of purchase,

through a negotiated sale with the Bureau of Treasury proved to be

problematic for the Treasury. The exclusive purchase offer would

have raised the local financial community's fears of a crony deal in

the making. This was primarily because the approval for such an

offer lies within the Department of Finance headed by Secretary Jose

Isidro Camacho, a brother of CODE-NGO chairperson, Maria Socorro

Camacho-Reyes. On July 12, 2001, National Treasurer Sergio Edeza

wrote a memo to Secretary Jose Isidro Camacho questioning the

propriety of issuing the bonds directly to CODE-NGO because CODE-NGO

was not a Government Securities Eligible Dealer. Sometime in

July/August 2001, Secretary Camacho hosts the infamous “meeting

between CODE-NGO and the Bureau of Treasury wherein both he and his

sister are present.

On September 26, 2001, it became

apparent that a negotiated sale was no longer possible when the

Bureau of Treasury announced that the PEACe Bonds will be sold via

auction to be held on October 2, 2001. As such, there was the

possibility that the bonds may not be issued to a single entity,

since there was a possibility that CODE-NGO may not win all of the

PEACe Bond issue.

Very Narrow Definition of the phrase

“at any one time”

Hence, there was a need for a third

clarificatory ruling that was made on September 29, 2001. In that

ruling, the BIR issued a ruling reiterated that the “the phrase 'at

any one time' covers only the origination or original issuance of the

bonds in the primary market regardless of whether sale or trading is

made in the secondary market.” It also stated that the determining

factor of whether or not the bonds were considered deposit

substitutes was the number of purchasers/lenders at the time of

origination/issuance.

It stated that:

“Corollarily, if

the proposed PEACe Bonds are issued to less than twenty (20)

individual or corporate lenders, the borrowing shall not be

considered as “public” borrowing. Hence, the instrument shall

not be classified as “deposit substitutes.” However, in the case

of PEACe Bonds, since the determining factor in ascertaining whether

or not such bonds are deposit substitutes is the original issuance to

more than twenty (20) individuals or corporate lenders, it holds to

say that the issuance to less than 20 individual or corporate lenders

will necessarily exclude them from the coverage of “deposit

substitutes.” Such being the case, the time element, i.e., “at

any one time” required in “public borrowing” shall not apply in

the instant case.”

The September 29, 2001 ruling also

removed the August 16 ruling's requirement that CODE-NGO/RCBC make a

representation/warranty that it was acquiring the bonds “for and on

its own behalf, or on behalf of a single purchaser only”

Implications of the 2001 Rulings

These BIR ruling is very crucial. By

defining the phrase “at any one time” to mean at the time the

PEACe Bonds were first auctioned off to the GSEDs, it allowed the

bonds to be sold in much smaller chunks in the secondary market

without losing its tax-exempt status. Furthermore, there was no need

to implement a tracking system to ensure that the bonds were held by

no more than 19 investors throughout the life of the bond.

If the ruling deemed the phrase “at

any one time” to mean for the life of the bonds, from date of

issuance to date of maturity, the bonds will have to be sold in no

more than 19 very large chunks of PHP 1.842 billion in face value or

over PHP 535.2 million in cash value (at the time of issuance). Any

investor who bought the bonds for resale at a later date will have to

find another investor with the cash to buy at least PHP 535.2 million

worth of PEACe Bonds in one transaction. That investor, in turn,

must have the willingness to hold the bonds until maturity (10 years

later) or have the capability to find another buyer just like him.

The “19-Lender Rule” was meant to be throughout the life of the

bond, it would severely limit the universe of potential bond buyers

to very large institutional buyers of which there are very few. The

limited market means that anyone who buys the bonds had better be

prepared to tie up a very large amount of cash until maturity (when

the bonds are repaid ten years later) if he is unable to resell the

bonds. This market invariably boils down to two types of investors:

Insurance Companies or other large

financial companies with similar long term obligations; or

Banks that need to fund the more

“permanent” core of their liquidity reserve requirements with

higher yielding instruments.

By eliminating the 19-Lender constraint

in the secondary market, the ruling vastly expanded the market for

PEACe Bonds without negating its tax-exempt status because the bonds

now had more uses.

Retail Products

It allowed for the creation of retail

products based on the zero-coupon bonds. According to RCBC Treasurer

Jaime Panganiban, RCBC has thought of creating “principal protected

products” not found locally.

“I can create

from these bonds a fund with a principal-protected product where your

upside potential is unlimited and your worse return is 100 percent of

your principal, because it's guaranteed by government, though we're

not saying we have advanced product knowledge because these products

you can easily find abroad,” he says.

Washing NPLs from a bank's own books

Since the bonds could now be sold in

much smaller chunks, the bonds could ostensibly sold down to the

level of a bank's own delinquent borrower and simultaneously be

repurchased from the borrower in a cashless debit-credit accounting

transaction that allows the borrowers delinquent loans to be

reclassified from an NPL to a receivable from the borrower that is

connected to the PEACe Bond and not the loan (See my previous post

http://systemisbroken.blogspot.com/2011/10/revisiting-peace-bonds.html

for a more detailed description of this process).

2004 and 2005 BIR Rulings

BIR's October 7, 2011 ruling was not

the first time the BIR reversed the 2001 PEACe Bond Rulings. The BIR

Rulings made in 2001 were first reversed in 2004 under BIR

Commissioner Guillermo L. Parayno (also of the Arroyo Administration)

by BIR Ruling No. 007-04 dated July 16, 2004, BIR Ruling No.

DA-491-04 dated September 13, 2004 and BIR Ruling No. 008-05 dated

July 28, 2005.

BIR's July 16, 2004 ruling (No. 007-04)

stated that:

“since the

object of the issuance is to obtain the required government funding,

the issuance and subsequent distribution (exchange and trading) of

Government debt instruments and securities in the secondary market to

other market participants, specifically, the investors, is in itself

a public borrowing of the government...It is, however, in the

secondary market that the investing public makes the indirect

investment in the borrowing entity, in this case, the Government.

...the mere

issuance of government debt instruments and securities is deemed as

falling within the coverage of “deposit substitutes” irrespective

of the number of lenders at the time of origination.”

...the phrase “at

any one time” in relation to public borrowing is deemed to refer to

the flotation of the debt instrument or security. In other words,

since the actual number of bondholders or investors may be at

maturity date of the financial instrument, more than 20 individuals

or corporation[s], the said direct lenders (origination) and indirect

investors (secondary market) are deemed to be what constitute

“public.”

Furthermore, the ruling stated that it

“effectively modifies and supersedes BIR Ruling Nos. 020-2001 dated

August 16, 2001 and DA-175-2001 dated September 28, 2001, as well as

other BIR rulings dealing on the matter.”

BIR Ruling No. DA-491-04 dated

September 13, 2004

This BIR ruling reiterated BIR Ruling

No. 007-04, stating that the matter of determining the number of

lenders does not come into play insofar as government debt

instruments and securities are concerned.” The ruling reinstated

the applicable provision of Revenue Regulations (Rev. Regs.) No.

17-84 which defined “deposit substitutes” to include “all

borrowings of the national and local government and its

instrumentalities... as evidenced by debt instruments denoted as

treasury bonds, bills, notes, certificate of indebtedness and similar

instruments...Consequently, the interest income derived therefrom by

the corporate or institutional lender shall be subject to the twenty

percent (20%) final tax imposed under Section 27(D)(1) of the Tax

Code of 1997.

BIR Ruling No. 008-05 dated July 28,

2005

This BIR ruling determined that the

twenty percent (20%) final tax is required to be withheld upfront.

Prospective or Retroactive? Or was it

overlooked?

It is unclear as to whether Rulings No.

007-04, DA-491-04, and 008-05 were meant to be applied retroactively

or prospectively. Given the lack of uproar at that time, it is safe

to assume that the ruling was presumed to be prospective. In a

petition before the Court of Tax Appeals, RCBC said that the BIR

itself signaled that the 2004 ruling will only cover future bonds.

It is also a distinct possibility that

this ruling may have been overlooked at the time it was issued

because the bondholders were not set to receive any imputed interest

income until the bond matured six to seven years later. The banks

affected claim to be utterly surprised by BIR's stance. However, BIR

Commissioner Kim Henares strongly doubts this: “I don't believe

that banks don't know about it because if you look at the history of

the trading of that bond, right after we issued the 2004 ruling, the

trading became markedly decreased.”

A chart of the PEACe Bonds trading volumes provided by the Philippine

Center for Investigative Journalism shows that trading in the bonds

dropped to almost zero after the BIR issued its July 16, 2004 ruling.

Trading only resumed in February 2006, but only sporadically and in

much smaller volumes.

BIR Ruling No. 370-2011 dated

October 7, 2011

The current BIR ruling states that BIR

Ruling No. 007-04 makes the case that the Tax Code is clear that:

“the term

“public” means borrowing from twenty or more individual or

corporate lenders at any one time,” wherein “the word 'any'

plainly indicates that the period contemplated is the entire term of

the bond, and not merely the point of origination or issuance.”

2001 Rulings Erroneous (or Anomalous?)

Furthermore, the current ruling stated

that the 2001 Rulings took the PEACe Bonds:

“out of the

ambit of deposit substitutes and exempting it from the 20% Final

Tax, an exemption in favour of the PEACe Bonds was created when no

such exemption is found in law. Thus, the 2001 Rulings are null and

void and cannot be given legal effect for being contrary to law. It

is a basic principle in administrative law that the interpretation

given by an administrative agency cannot run contrary to the law

which it seeks to implement.”

The current ruling deemed 2001 Rulings

erroneous but given the other controversial aspects of the PEACe

bonds such as the information asymmetry, the wide bids, the vast gap

in YTMs at the point of auction to the point of sale to institutional

investors, the purported cronyism, it is easy to think of this

“error” as anomalous.

The ruling went on to state that

CODE-NGO should be held liable to pay the 20% Final Tax on interest

income it realized from its purchase of the PEACe Bonds. Had CODE-NGO

paid this tax at the time of issuance, it would have paid PHP 1.4

billion in addition to the PHP 10.169 billion purchase price of the

PEACe Bonds. But since no final tax was paid by CODE-NGO upon

issuance of the PEACe Bonds, CODE-NGO is liable to pay 20% final tax

on the entire PHP 24.3 billion discount, or approximately PHP 4.86

billion.

Retroactivity

The ruling said that CODE-NGO/RCBC may

not invoke the principle of non-retroactivity because Section 246 of

the 1997 Tax Code allows for retroactivity in cases where:

the taxpayer deliberately

misstates or omits material facts from his return or any document

required of him by the Bureau of Internal Revenue;

the facts subsequently gathered by

the Bureau of Internal Revenue are materially different from the

facts on which the ruling is based; or

the taxpayer acted in bad faith.

The BIR said that there is:

“ample legal

authority to conclude that the non-retroactivity principle does not

apply when the ruling involved is null and void for being contrary to

law, such as the 2001 Rulings. Well-entrenched are the principles

that the Government is never estopped from collecting taxes because

of mistakes and errors of its agents and there are no vested rights

in a wrong interpretation of the law.”

Wrong Target

Although the ruling found CODE-NGO

liable for PHP 4.86 billion in taxes, it decided to collect this tax

by withholding 20% of the PEACe Bonds imputed interest income prior

to its payment on the maturity date. Since neither CODE-NGO nor RCBC

holds the bonds, the parties affected will be the final bondholders,

in other words, those institutional investors who bought the bonds in

the secondary market after CODE-NGO/RCBC had sold them down.

The Department of Finance issued two

directives which compounded the problem:

The Department of Finance issued a

Memorandum dated October 11, 2011 which barred the sale and transfer

of the PEACe Bonds from October 12, 2011 until the bonds were

redeemed on October 18, 2011. Institutional investors who were

uncomfortable with the October 7, 2011 ruling could not rid

themselves of the PEACe Bonds they held.

The BIR issued Ruling No.

DA-378-2011 dated October 17, 2011 which revised the previous

October 7, 2011 ruling to withhold the taxes due not only from

CODE-NGO/RCBC but also to all subsequent bondholders. As a

consequence, all subsequent bondholders were made liable for the 20%

Final Tax.

Left Holding

the Bag

A total of nine banks have reportedly

been adversely affected. Eight of these banks, namely Banco De Oro,

Bank of Commerce, China Banking Corporation, Metropolitan Bank &

Trust Company, Philippine Bank of Communications, Philippine National

Bank, Philippine Veterans Bank, and Planters Development Bank, have

petitioned the Supreme Court to annul the October 7, 2011 BIR Ruling.

The ninth, BPI Family Bank, declined to participate in the petition

but stated that it held around 5% of the PEACe bonds.

RCBC, in a separate petition, also questioned the propriety and

legality of the BIR ruling

but did not indicate as to whether it still held some PEACe Bonds.

The eight banks asked for and received

the immediate issuance of a temporary restraining order (TRO) and/or

Writ of Preliminary Injunction. The PHP 4.86 billion tax to be

withheld was placed in escrow while the balance of PHP 30.14 billion

was paid out to the bondholders. The banks have argued that the

imposition of the 20% Final Tax on the PEACe Bonds was:

“extremely

prejudicial to the bondholders, including petitioners who relied in

good faith on the BIR declaration that the bonds are exempt from

final tax...Such unilateral imposition of the 20 percent final

withholding tax on the interest/discounts realized on the government

bonds only on the eve of its maturity with nary any prior

consultation with the petitioners and other bondholders also amounts

to confiscation of the petitioners’ property without due process...

Threatened refusal of the government to pay the full face value of

the government bonds to its contractual undertaking and material

representation at the time of their issuance, operates as a fraud on

investors to their grave or irreparable injury or prejudice, which,

in turn, adversely affects their perception of the Philippines as an

investment destination,”

According to the petitioning banks:

“The

repercussions of the Government's threatened intent of reneging on

its commitment on the Government Bonds have far-reaching implications

which are too important to ignore. There will be heightened

perception that the Philippine Capital Markets are volatile and

unpredictable...The Government will suffer from damaged credibility

in terms of investor confidence (whether current or prospective,

local or foreign) relative to the legitimacy of its commitments

which, by reason of the 2011 BIR Ruling, may now be perceived as

subject to arbitrary reversals and/or modifications.”

The petitioning banks also added that

the unilateral amendment of a material term of the contract between

the bondholder and the government was never agreed to by the

petitioners, thus a violation of the contract. Moreover, the

imposition of a 20% Final Withholding Tax (FWT) on the eve of the

bond's maturity was done “without any prior consultation with the

petitioners and other bondholders or a hearing amounted to

confiscation of the petitioners' property without due process.”

Flawed Ruling

There are also strong indications that

BIR did not give a lot of thought to the mechanism of collecting back

taxes on the PEACe Bonds. BIR collection mechanism is flawed

because:

Final Bondholders

It extracts the back taxes from

the funds that will be remitted to the final bondholders upon

maturity, while the main beneficiaries and proponents of the

erroneous 2001 rulings, namely CODE-NGO and RCBC, get away

Scot-free.

Moreover, the ruling extracts the

20% FWT irregardless of the length of time the bond was held.

Therefore, it disproportionately punishes the more recent

bondholders who will bear brunt of the taxes even though they earned

the least of the imputed interest. As an example, an investor who

decided to park PHP 1.0 million of his money in the supposedly

risk-free PEACe Bonds for a month or two before maturity will lose

14.19% of his principal even though he earned a few months of

imputed interest. Similarly, because the ruling takes away 14.19% of

the bond's redemption proceeds at maturity irregardless of the

bondholder's holding period, an investor who bought the bonds at its

accreted value one year before its maturity will lose 2.92% of his

capital instead of earning the expected 12.75% YTM on the bond.

Those bought the bonds at their accreted value and who held the

bonds longer will only lose the imputed interest and not principal.

Given that

interest rates have gone down substantially since 2001, the bonds

were most likely purchased at a premium to their accreted values,

therefore it is highly likely that investors who have held the bonds

for less than four years will suffer a loss of principal as well.

Subsequent

Bondholders

Under BIR Ruling

No. DA 278-2011 dated October 17, 2011, the BIR has found

“RCBC/CODE-NGO” and “all subsequent holders” of the PEACe

Bonds liable for the 20% FWT. This implies that the 20% FWT may be

netted out from the sale and resale of the bonds and that the

bondholder may only be liable for the taxes on the imputed interest

accreted during the time the bond was held by the investor. In other

words, an absolute 20% FWT becomes a 20% FWT proportionate to the

imputed interest earned by the bondholder.

This arrangement

is more equitable to the final bondholders. The 20% FWT would only

then cut into the imputed interest earned by the bondholder over the

life of his holding period and not into the principal, whether or not

the bond was purchased at its accreted value or at a premium to its

accreted value.

Under an absolute

20% FWT, the bond's 12.75% YTM would now range from 11.13% YTM if the

bonds were bought at time of issuance to -14.19% YTM if the bonds

were bought right before maturity. If the 20% FWT were proportionate

to the imputed interest earned, the bond's revised YTMs would not

decline so drastically: from 11.13% YTM if the bonds were bought at

time of issuance to 10.26% YTM if the bonds were bought right before

maturity.

Collection Problem

However, there is

a problem with this scenario: The government claims it does not even

know who the final bondholders are unless they come forward to claim

the redemption proceeds of the bond at maturity date (although the

Registry of Scripless Securities “RoSS” under the Bureau of

Treasury is primarily tasked with monitoring and maintaining official

records of ownership of government securities). According to BIR

Commissioner Kim Henares:

“We don't have

the list of the banks holding the PEACe Bonds. Supposedly under the

bank secrecy law, it is supposed to be confidential. The instruction

is to hold the 20% of the PHP 25 billion,”

If this is the

case, only the final bondholders would be affected. Unless the

government recreates the chain of sale and resale from CODE-NGO/RCBC

to the final bondholders, the final bondholders would have to

recreate this process via a chain of litigation, meaning the final

bondholder would have to sue the previous bondholder to collect the

20% FWT that the final bondholders are not liable for, and that

previous bondholder would have to collect from the previous

bondholder, and so on and so forth, until the chain of sale is

retraced back to CODE-NGO/RCBC, the original bondholders. Needless

to say, this would create a gigantic legal mess.

The only advantage to the current

ruling is that it reduces the cash outflow of the government by 20%.

But in the long run it will turn off potential investors because the

bond buyers, who bought the bonds in good faith, were harmed and the

bonds themselves did not prove risk free. In the future, buyers of

government securities will attach a higher risk premium to government

debt, especially government debt securities with all the extra

features, to compensate themselves for the regulatory risk that the

government will rescind these embellishments when the bonds mature,

leading to higher interest rates for the entire country.

The BIR should have assessed

CODE-NGO/RCBC for the PHP 4.86 billion in back taxes which would have

wiped-out the endowment of the PEACe Foundation and put a big dent in

RCBC's earnings and capital. But the ruling would not have angered

the rest of the investment community and the country would not have

to pay for the arbitrariness of the ruling in terms of higher debt

costs. No one else but CODE-NGO/RCBC would have been affected and

given how controversial the transaction is perceived to be even ten

years later, the action would have been seen as just.

Impact on Bank's Bottom Line

The surprise imposition of the 20%

Final Withholding Tax will affect the bottom line of the banks. None

of them have properly accrued for the presumed tax liability and none

of them have prepared themselves to receive less cash from the

redemption payment of the PEACe Bonds.

To assess this impact, an analysis was

made of the affected bank's holdings of government debt securities.

With the exception of BPI Family Bank (who already disclosed

ownership of 5% of the PEACe Bonds),

the analysis makes a critical assumption that each bank's PEACe Bonds

holdings would be proportionate to their holdings of government debt

securities as indicated in their latest available audited financial

statements.

Under

this scenario, the most adversely affected bank is Planters

Development Bank with a 4.92% hit to their capital base, followed by

Philippine Bank of Communications, with a 3.43% hit to capital,

followed by Philippine National Bank (2.42% hit), and China Banking

with a 2.06% hit to their capital. Of course, depending on the

circumstances, each bank may have much higher or much lower PEACe

Bonds holdings than dictated by their government debt securities

holdings. So this analysis, with the exception of BPI Family bank, is

just a guesstimate.

Affected

Banks

Analysis

of Impact of 20% Final Withholding Tax

on

Affected Bank Capital

As of December 31, 2010

|

Bank

|

Total

Holdings of Government Debt Securities

(In PHP

B)

|

%

|

PEACe

Bonds Holdings

(In PHP

B)

|

FWT

Due

(In PHP

B)

|

Capital

Funds

(In

PHP B)

|

Capital

Affected

(In %)

|

Banco

De Oro

|

143.26

|

29.58%

|

10.200

|

1.416

|

88.302

|

1.60%

|

Bank

of Commerce

|

14.178

|

2.93%

|

1.010

|

0.140

|

14.569

|

0.96%

|

BPI

Family Bank

|

17.279

|

3.57%

|

1.750

|

0.243

|

12.564

|

1.93%

|

China

Banking Corporation

|

67.007

|

13.84%

|

4.77

|

0.663

|

32.221

|

|

Metropolitan Bank and Trust Company

|

143.690

|

29.67%

|

10.232

|

1.421

|

95.772

|

1.48%

|

Philippine

Bank of Communications

|

13.988

|

2.89%

|

0.996

|

0.138

|

4.033

|

3.43%

|

Philippine

National Bank

|

69.906

|

14.44%

|

4.978

|

0.691

|

28.527

|

2.42%

|

Philippine

Veterans Bank

|

8.583

|

1.77%

|

0.611

|

0.085

|

5.391

|

1.57%

|

Planters

Development Bank

|

6.345

|

1.31%

|

0.452

|

0.063

|

1.276

|

4.92%

|

Total

|

484.234

|

100.00%

|

35.000

|

4.860

|

282.656

|

1.72%

|

These five, as indicated in

the table below, have a high amount of Non-Performing Assets or

Distressed Assets on their balance sheets relative to their Total

Capital Cushion, which is their ability to absorb losses from the

deterioration of the value of their Distressed Assets. These five,

namely Bank of Commerce, Philippine Bank of Communications,

Philippine National Bank, Philippine Veterans Bank, and Planters

Development Bank, have a Distressed Assets to Total Capital Cushion

Ratio greater than 100%, which indicates a heightened risk of

insolvency. A sixth bank, namely BPI Family Bank, has a ratio of

93.73%, which is borderline close to the 100% danger line.

Affected Banks

Distressed Assets to Total Capital Cushion

As of June 30, 2011

|

|

Total

Distressed Assets

(In PHP B)

|

Total

Capital Cushion

(In PHP B)

|

Distressed Assets/

Total Capital Cushion (In %)

|

| Banco De Oro Unibank |

66.86

|

109.86

|

60.86%

|

| Bank of Commerce |

34.08

|

18.57

|

183.54%

|

| BPI Family Bank |

11.78

|

12.56

|

93.73%

|

| China Banking Corporation |

18.93

|

35.38

|

53.51%

|

| Metropolitan Bank and Trust Co. |

61.2

|

91.21

|

67.10%

|

| Philippine Bank of Communications |

9.6

|

6.1

|

157.41%

|

| Philippine National Bank |

67.33

|

38.26

|

175.98%

|

| Philippine Veterans Bank |

10.79

|

6.1

|

176.82%

|

| Planters Development Bank |

13.53

|

3.76

|

360.14%

|

| Total |

294.1

|

321.8

|

91.39%

|

NPL Washing

The high incidence of distressed and

near distressed banks (six out of nine banks) indicates that these

banks may have used the PEACe Bonds for their ability to “window

dress” bank NPLs (see a previous October 7, 2011 post “Revisiting

the PEACe Bonds under the section “What else can RCBC do with the

PEACe Bonds?,

http://systemisbroken.blogspot.com/2011/10/revisiting-peace-bonds.html).

Most likely, the affected banks used

the PEACe Bonds to wash NPLs from their own books in cashless

debit-credit accounting transactions.

From “What else can RCBC do with the

PEACe Bonds?:

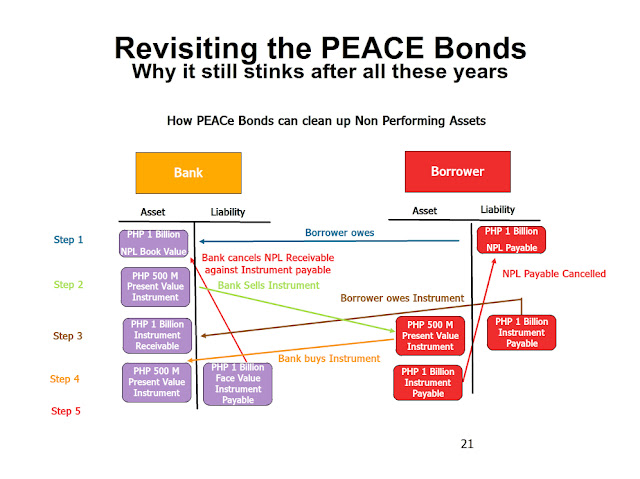

For instance, an

NPL that is on the bank's books for PHP 1.0 billion may only have a

recoverable value of PHP 500.0 million (Step 1). The bank can sell a

PHP 1.0 billion Face Value PEACe Bond (with a discounted value of PHP

500.0 million) to the delinquent borrower (Step 2). But on the books

of both the bank and the delinquent borrower, the amount owed to the

bank is recorded at the face value of the PEACe Bond, which is PHP

1.0 billion (Step 3). The bank then simultaneously buys back the

PEACe bond from the delinquent borrower (Step 4). The repurchase of

the PEACe Bond creates a payable on the right side of the bank's

balance sheet and puts the bank in a situation where its has itself a

shadow indebtedness to the borrower in the same exact amount as the

NPL. The bank then offsets its account payable to the borrower

against the NPL (of the same amount) of the delinquent borrower on

the asset side (Step 5). This way, the indebtedness of the borrower

remains on the accounts receivable portion of the asset side of the

bank's balance sheet but it is no longer an NPL and is not connected

to a loan. Thus the bank's balance sheet is laundered in a way by

simply removing the stain of non-collectibility or ageing. The new

receivable derived from the sale and repurchase of the PEACe Bond is

after all exactly that - new.

Overstated Capital

Although the estimated impact of the

abrupt imposition of the 20% FWT on bank capital is estimated to be

only a 1.72% reduction in bank capital, five of the banks in question

are distressed and their capital is already overstated. In some

cases, the overstatement is so severe, that any additional reduction

in capital from the 20% FWT may severely impair the bank's actual

capital beyond the point of solvency. (See “BSP's Ampaw Accounting

System”

http://bancofilipinofailure.blogspot.com/2011/09/bsps-ampaw-accounting-system.html)

The reason for the overstatement is

that the BSP has granted regulatory relief to these banks and allowed

them to:

Defer the booking of realized

losses arising from:

The Sale of Non-Performing Loans

to Special Purpose Vehicles (SPVs);

The Acquisition by a Bank of Bank

of another weaker Bank with substantial Non-Performing Assets;

Large Credit and Impairment Losses

on financial assets of banks that are undergoing a BSP-approved

Rehabilitation Plan

Amortize the realized losses over

a period of 10 to 20 years

As a result of this regulatory relief,

losses were not realized on these banks books. Instead, the

unrealized losses were swept into the “Other Assets” accounting

bucket as deferred charges. Although the BSP mandated regulatory

relief allowed the banks to look stronger than they are, such

bookings do not comply with Philippine Financial Reporting Standards

(PFRS). As a result, banks that availed of the regulatory relief

show a qualified auditor's opinion that:

States that the bank's booking of

deferred charges does not comply with the provisions of

GAAP/PFRS/PAS

Discloses the impact such

compliance would have on the bank's financial statements had the

losses been recognized.

Banks with Qualified Auditor's Opinions on

Deferred Charges

As of December 31, 2010

|

Bank

|

Deferred Charges

|

Unadjusted Capital Funds

|

Adjusted Capital Funds

|

% Reduction in Capital Funds

|

| Bank of Commerce |

PHP 4.4 B

|

PHP 7.6 B

|

PHP 3.2 B

|

57.90%

|

| Philippine Bank of Communications |

5.9 B

|

3.6 B

|

-2.3 B

|

163.90%

|

| Philippine National Bank |

5.6 B

|

33.3 B

|

27.7 B

|

16.80%

|

| Philippine Veterans Bank |

1.1 B

|

5.0 B

|

3.9 B

|

21.70%

|

| Planters Development Bank |

1.6 B

|

3.7 B

|

2.1 B

|

43.20%

|

| Total |

PHP 18.6 B

|

PHP 49.6 B

|

PHP 34.6 B

|

30.24%

|

Conclusion

Although the Aquino Administration has

given some thought as to the errors of the 2001 Banez rulings on the

PEACe Bonds, it seems that it has not given much thought as to the

methods by which these “errors” could be rectified. Instead of

targeting CODE-NGO/RCBC, the main beneficiaries and proponents of the

2001 rulings, for collection of unpaid taxes, it chose to extract

these back taxes from the final bondholders. More so, it did this

in a manner that disproportionately punishes the the investors who

acquired the bonds on a more recent basis. The 2011 BIR rulings are

undoubtedly flawed. As to whether they will weaken an already

weakened banking system remains to be seen. But they have already

achieved the unintended consequence of seriously damaging the

government's credibility not only with regards to the sanctity of its

contractual obligations but also with regards to its ability to

thoroughly think through the ramifications of its decisions.